Venison Market Analysis: 2021–2025

Contributed by Zadia Lubbe – Beyond Bush Venison

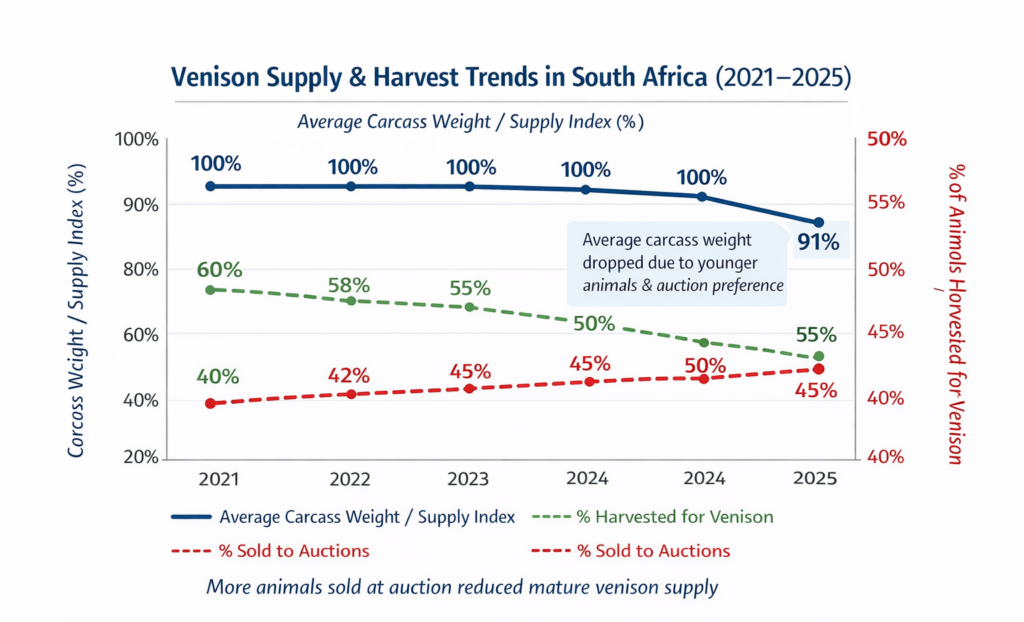

The venison market between 2021 and 2025 reveals a sector undergoing a deep structural transition—one shaped not simply by biological cycles, but by the shifting economics of South Africa’s wildlife industry. For most species, carcass weights remained relatively stable through 2021 to 2024, creating the impression of a steady, predictable supply environment. Yet beneath this stability, powerful forces were already reshaping the market. By the time the sector entered 2025, these underlying pressures had become unmistakable.

Across all species, the average carcass weight declined sharply—by approximately 9%—from 2024 to 2025, signalling a material shift in the age profile of harvested animals. Hunters and landowners alike reported increasing difficulty in finding mature game, as the industry-wide shortage of wildlife began influencing venison supply. Animals were increasingly being harvested at younger ages, long before they reached their full biological mass. This contraction in carcass weight was not an isolated trend: it was the visible consequence of a deeper disruption in the balance between live-auction value and meat-market supply.

Through 2022, 2023 and 2024, the wildlife economy experienced a significant uplift as auction prices strengthened across virtually all plains species and many variants. What followed was a notable behavioural shift among landowners. With live-sale returns rising sharply, the incentive to harvest animals for venison weakened. Instead, breeders and wildlife managers diverted stock toward auctions, where even mid-tier species began generating stronger returns than their venison equivalents. As a result, culling volumes declined and fewer mature animals entered the venison supply chain.

This tightening of supply was then compounded by changes in international hunting behaviour. As auction prices rose and safari packages effectively held their price ceilings, visiting hunters were able to take fewer animals for the same spend, reducing the throughput of mature carcasses even further. The venison market entered 2025 with a combination of lower volumes, lighter carcasses and reduced age diversity—conditions that inevitably pressured both market value and industry confidence. Indeed, venison value contracted by more than 20% from 2024 to 2025, signalling a significant cooling after earlier years of gradual growth.

Pre-2024 data, however, paints a very different picture—one where venison and auctions still operated as two economically viable and complementary pathways, giving landowners real flexibility in how they utilised specific species. Zebra is an excellent example. With an average carcass weight of around 140 kg, venison returns of approximately R3 500 made harvesting a rational option on many properties. Meanwhile, pre-2024 auction prices hovered near R3 850 after capture costs, offering an alternative but not overwhelmingly superior avenue for income generation. The defining feature of this period was balance: landowners could comfortably choose between the two markets based on veld load, herd management objectives and seasonal demand.

Giraffe reflected this same dual-pathway flexibility. Venison values of roughly R13 500 per carcass, supported by an average carcass weight of 540 kg, provided a strong incentive to harvest mature animals, while auction returns after capture costs of approximately R12 600 offered a credible alternative. Because neither pathway dominated decisively, landowners were able to align utilisation decisions with ecological and commercial priorities. Prior to 2024, both venison-based utilisation and auction-based realisation were economically defensible, enabling a diversified and resilient management strategy.

As the industry moved into 2024—and especially 2025—this balance collapsed. Auction prices accelerated sharply across multiple categories, while carcass weights and venison throughput deteriorated. What had once been a genuine choice became an increasingly one-sided equation: selling live animals yielded far superior returns, while harvesting for venison delivered diminishing value. This drove an industry-wide pivot away from venison and toward auctions, which—while economically rational—left the venison sector with reduced supply, reduced maturity and contracting output.

Red Meat Inflation and the Resulting Demand Pressure on Venison

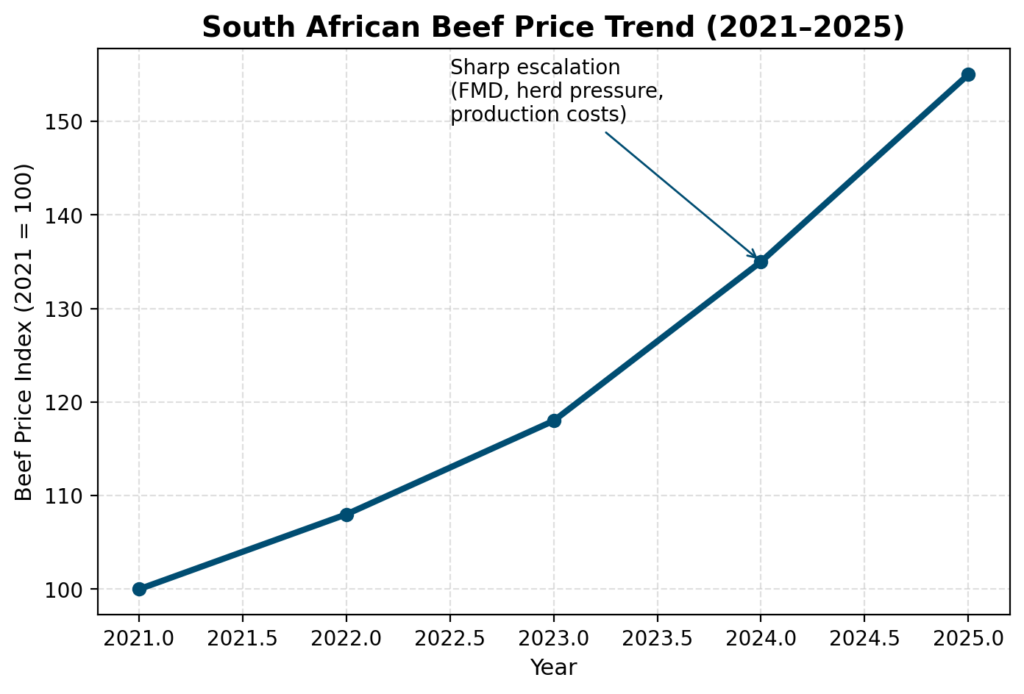

The sharp escalation in beef prices from 2024 into 2025 materially altered demand dynamics across the broader red meat sector. As beef prices rose—driven by Foot and Mouth Disease (FMD), constrained herd numbers and rising production costs—processors and consumers increasingly sought cost-effective alternatives to traditional beef inputs. In this environment, Venison trimmings emerged as a natural substitute, particularly in secondary processing, manufacturing and value-added product categories.

Unlike premium whole-muscle cuts, trimming markets are highly price-sensitive. As beef trimming prices increased, demand shifted toward venison trimmings, which historically offered a more affordable red protein with acceptable functional and sensory characteristics. From a demand perspective, rising beef prices therefore strengthened interest in venison. The venison market entered 2025 with a structurally supportive demand environment driven by red meat inflation.

However, this demand increase coincided with a pronounced contraction in venison supply. From as early as 2024, reduced harvesting volumes—driven by elevated auction prices and declining availability of mature animals—began limiting venison throughput. By 2025, lower carcass weights, reduced age diversity and fewer animals entering the meat channel significantly constrained the availability of venison. As a result, the industry faced a classic supply–demand imbalance: demand strengthened precisely as supply deteriorated.

This imbalance had important implications for price formation within the venison market. While realised venison values declined in aggregate during 2025 due to lower volumes and lighter carcasses, underlying demand for specific components—particularly trimmings—outpaced available supply. In economic terms, venison prices had not yet fully adjusted to reflect this new scarcity. The market was absorbing supply-side contraction faster than it was recalibrating price signals.

In a normalising market environment, sustained demand pressure combined with constrained supply would necessitate upward price adjustment in venison, particularly for trimming categories that directly compete with beef inputs. The reluctance or delay in price realignment during 2025 can be attributed to transitional market behaviour, fragmented supply, and lingering perceptions of venison as a secondary protein rather than a structurally scarce one.

Conclusion:

The implication is clear: as long as beef prices remain elevated and venison supply remains constrained, the economic case for higher venison pricing strengthens. Without price correction, the venison market risks chronic undersupply, reduced processor participation, and continued erosion of value chain confidence. Adjusting venison prices to reflect true scarcity is not only economically rational but also necessary to restore balance between demand, supply, and sustainable utilisation.

In this context, the venison market’s challenge is no longer one of demand creation but of aligning price, supply, and utilisation strategies in a red meat environment where alternative proteins are increasingly sought after yet biologically limited in their capacity to expand output rapidly.